January 2026 Market Update

2025 is done and 2026 is here. We’ll take a brief look back at the final month of 2025 and the real estate activity (Residential Sales). We’ll have a more detailed yearly review in another post.

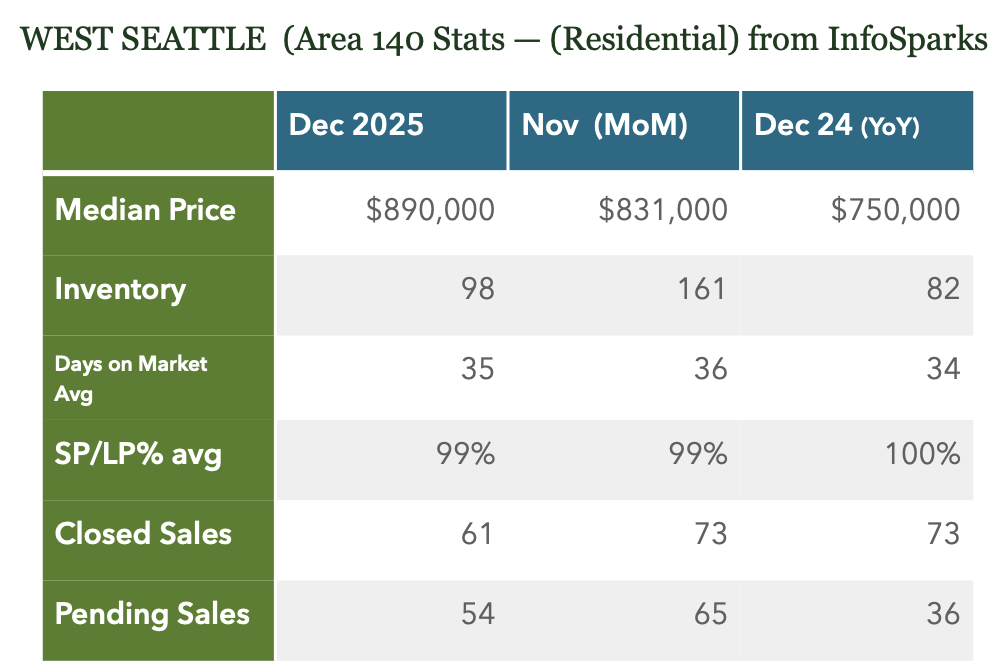

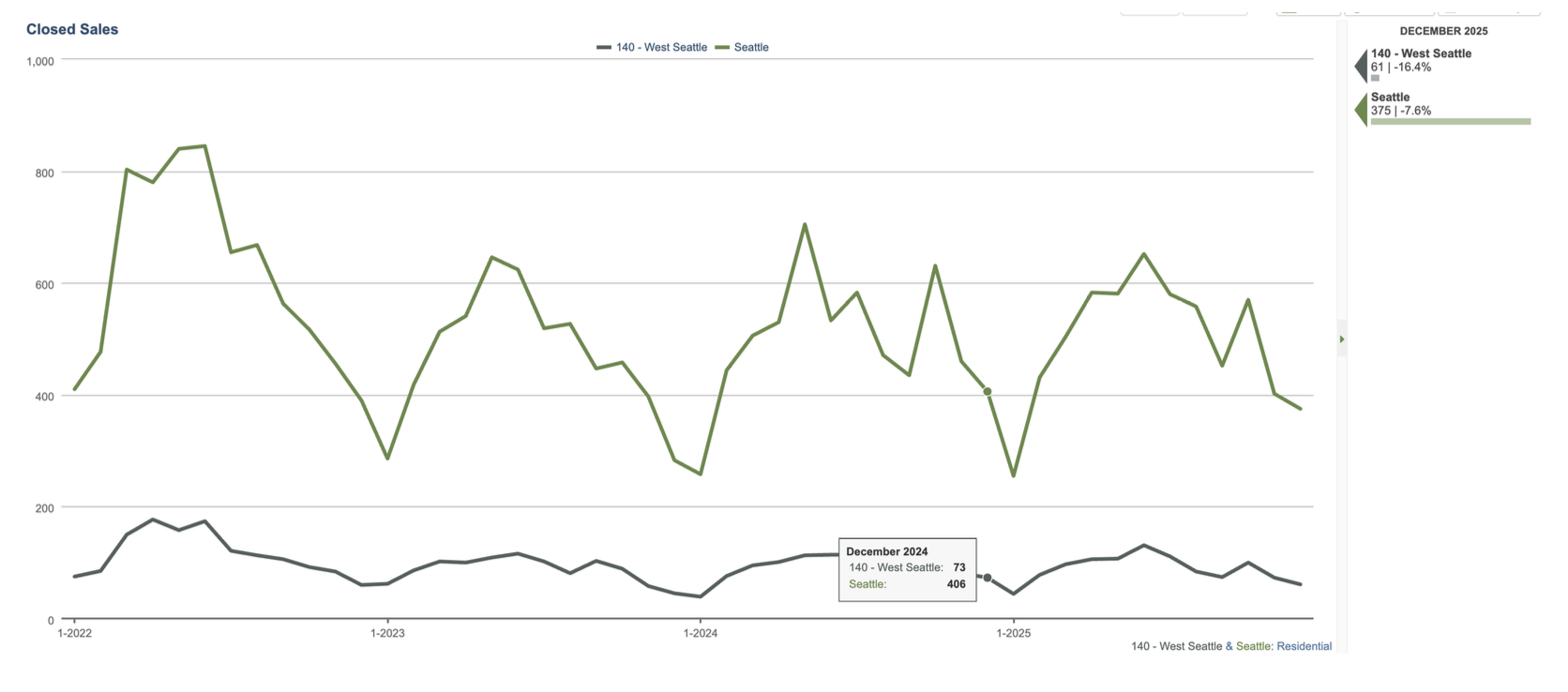

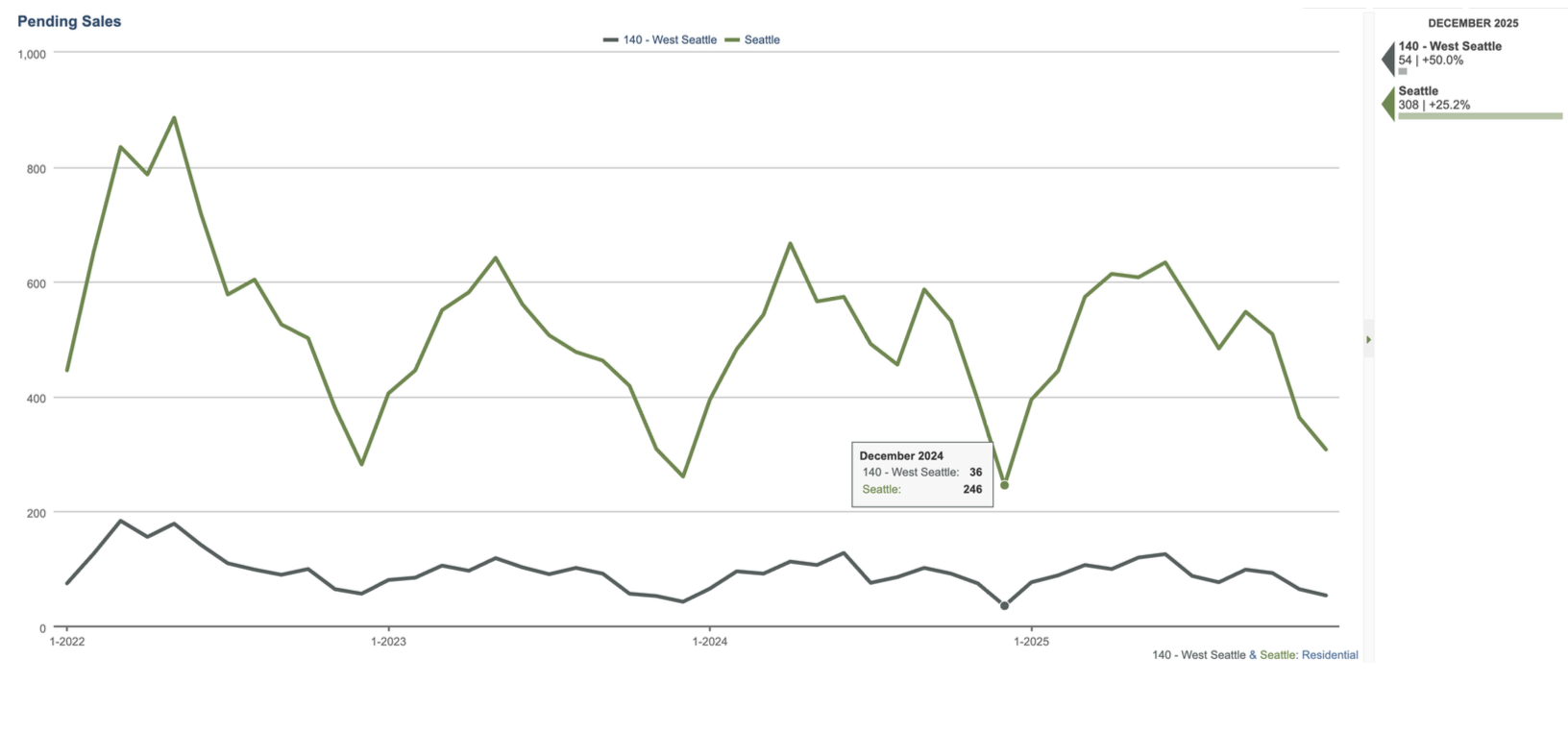

December is typically a slower month for home buying and selling and last month followed that trend. There were 61 closed sales, compared to 73 in November. June ‘25 was peak sales month at 131 closed sales for reference. Median price was up Month-Over-Month at $890,000 (831k in November) so the homes that did close were in the higher pricing tiers. A specific month’s recorded closing sales often come from the previous month’s pending sales. November had 63 Pending sales so some of those are represented in this number (December had 54 pending sales). Inventory dropped to just under 100 homes. There were 191 homes on the market at the end of October, so this is big drop. The drop can be partially attributed to homes getting accepted offers, homes being taken off market (canceled listings or off-market for holidays) and not a lot of listings came to market in December. There were only 26 New Listings last month (vs. 154 in September of 2025). This low number is pretty typical as we see sellers waiting for better market timing (early part of the year). Sales Price-List Price Ratios were at 98%, so there was some price concessions.

These sales numbers pretty much followed seasonal norms. We’d expect January numbers to follow before taking off Late-Winter/Early Spring. Historically, the regional market takes off right after the Super Bowl (or after the Seahawk’s season finishes). It probably has to do more with better weather, Buyer’s renewed urgency after the new year and Seller’s strategically listing (in a market with more demand and less inventory). We historically see New Listings start to come out over January-February but really peak after spring break through June.

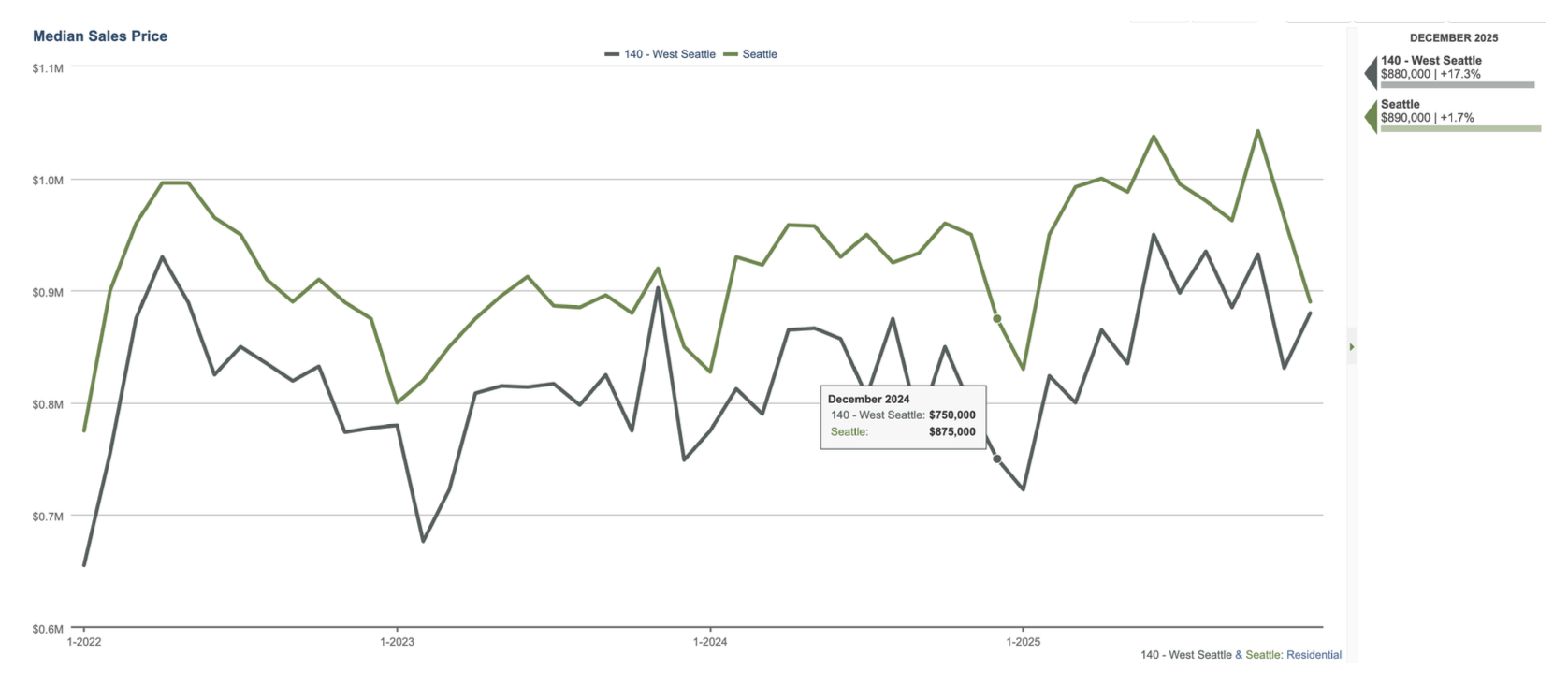

Median Sales Price - Median Price was up Month-Over-Month at 890k which is pretty close to the overall 2025 West Seattle Median, 880k. The closed sales in December had more higher tier prices, including 15 sales over 1M (and the most expensive home closing in December at 2.295M). Last year’s Median in December was 750k, so it seems buyers are out there and willing to purchase homes. Only 8 of the 61 closed sales had over 100% List Price-Sales Price Ratios, so there were less escalators. 27 sales sold for less than 100% of Sales Price. There could be some other concessions (lender or closing cost credit or inspection concession) not reflected in the price.

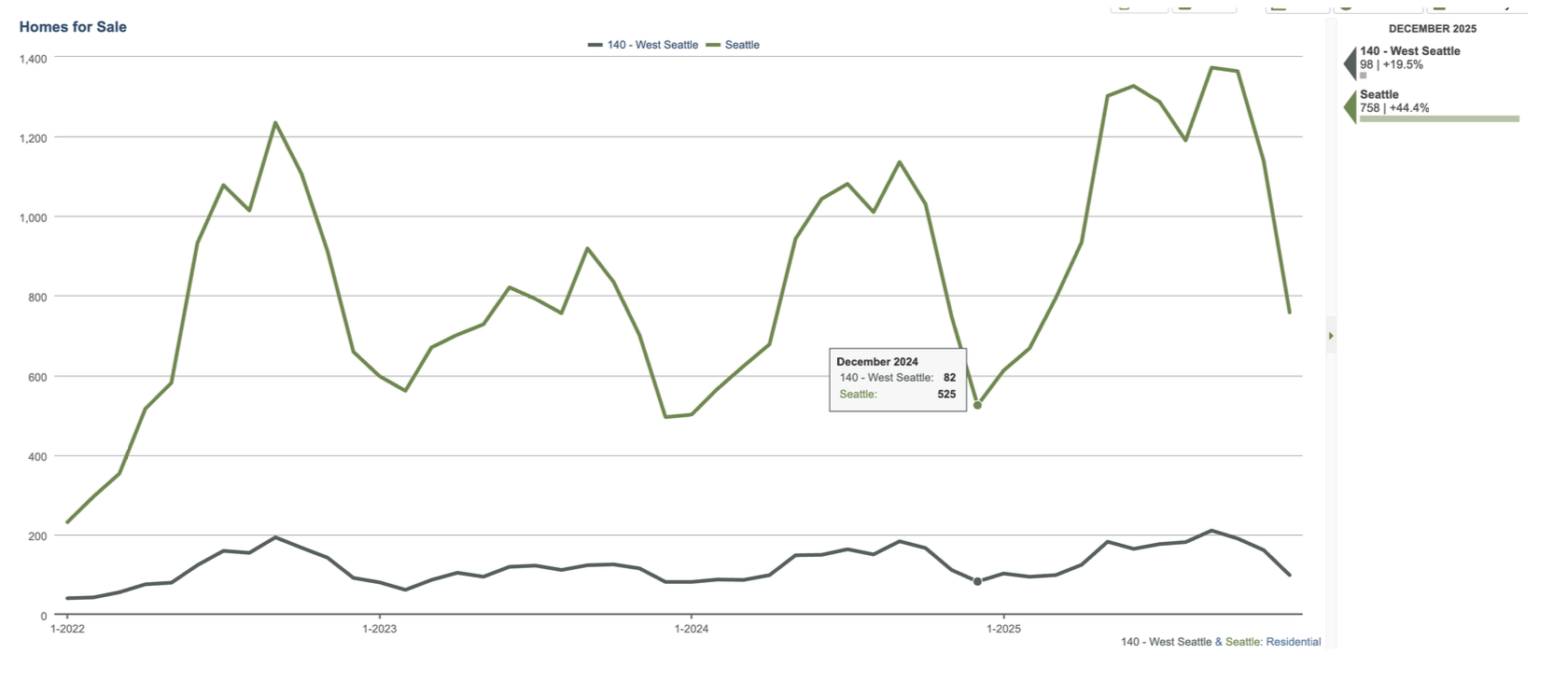

Homes for Sale - Inventory followed seasonal trends and dropped to 98 available homes. This is likely due to sales of homes and not a lot of new entries to the the market. We had seen 154 New Listings in September and 116 in October but only 76 in November and 26 in December. So, most of the new inventory got absorbed and not a lot took its place. In addition, we saw 34 properties get cancelled, go temporarily off-market or expire last month. We likely will see some of these homes come back to market in the upcoming weeks.

Sold Sales - There were 61 sold properties last month. Looking at the below chart, you can see this follows seasonal trends. There is less inventory and buyers so makes sense. The past 3 years have had fairly consistent patterns. The early part of 2022 was the last year of low interest rates. Rates have hovered in the low 6’s for the past month or so, down from almost 7% a year ago. Most experts think rates should remain at this level most of the year.

Pending Sales - 54 homes went under contract last month, slow from years peak but better than a year ago. We’d expect these number to pick up as we move through the beginning of 2026.

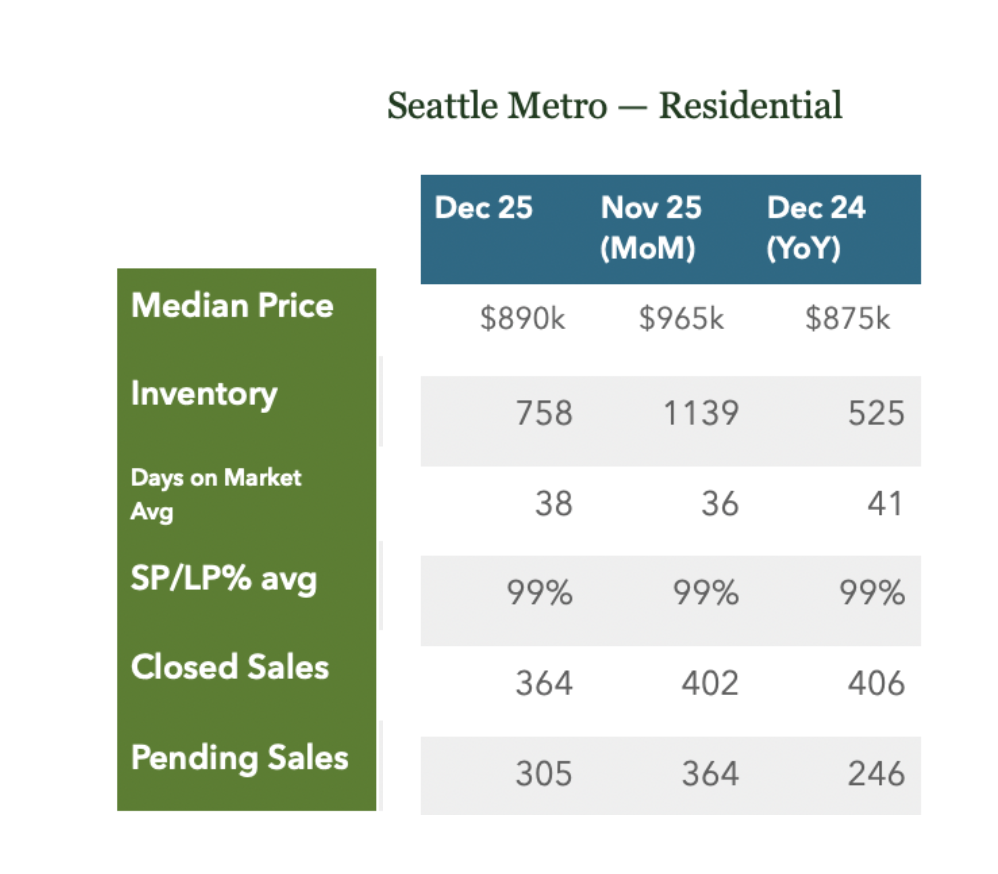

Seattle Metro - Median finally went below 1 Million the past 2 months. The Median had peaked at $1,042,000 in October (previous high had been $1,037,000 in June). This is typically reflective of the previous month’s activity, so reinforces Spring (April-May) and early fall (September) as the most active, expensive times in the market. Seattle Metro saw drops in inventory, closed sales and pending numbers last month. We’d expect all those to pick up next month or February.

Of note, 314 of the 758 available homes are considered New Construction. These would likely be Townhomes, ADU/DADU, attached residential homes. 314 represents a 61% increase from the December 2024, when there were only 194 of these styles of homes available. There has been a big increase in New Construction inventory this year.