March 2026 Market Update

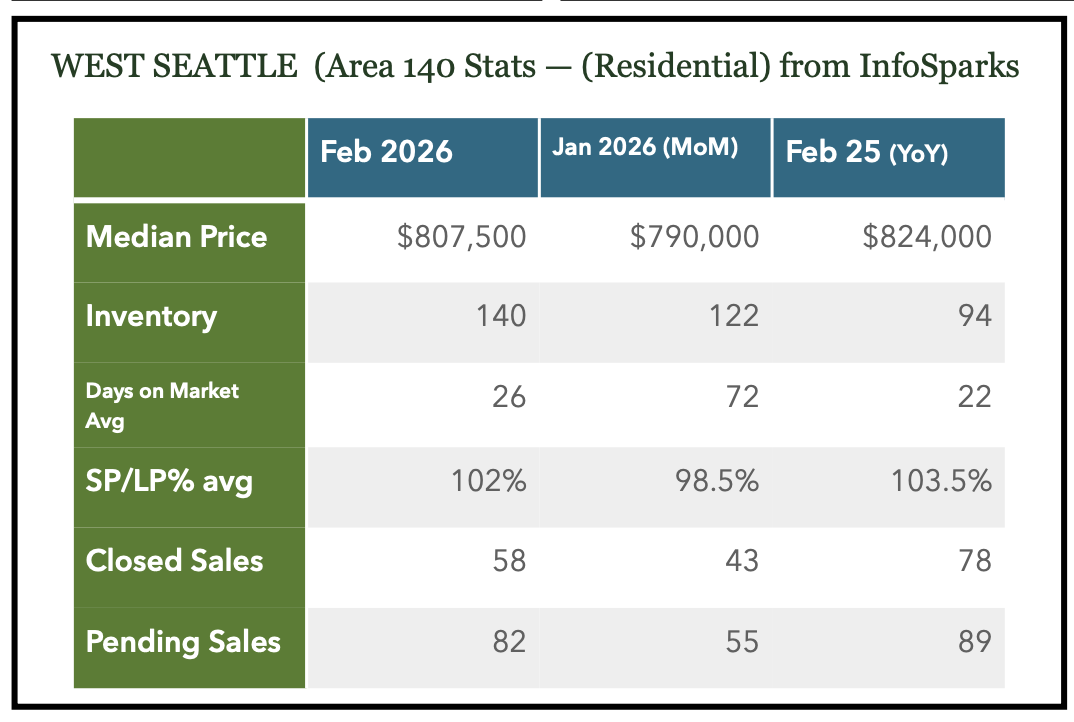

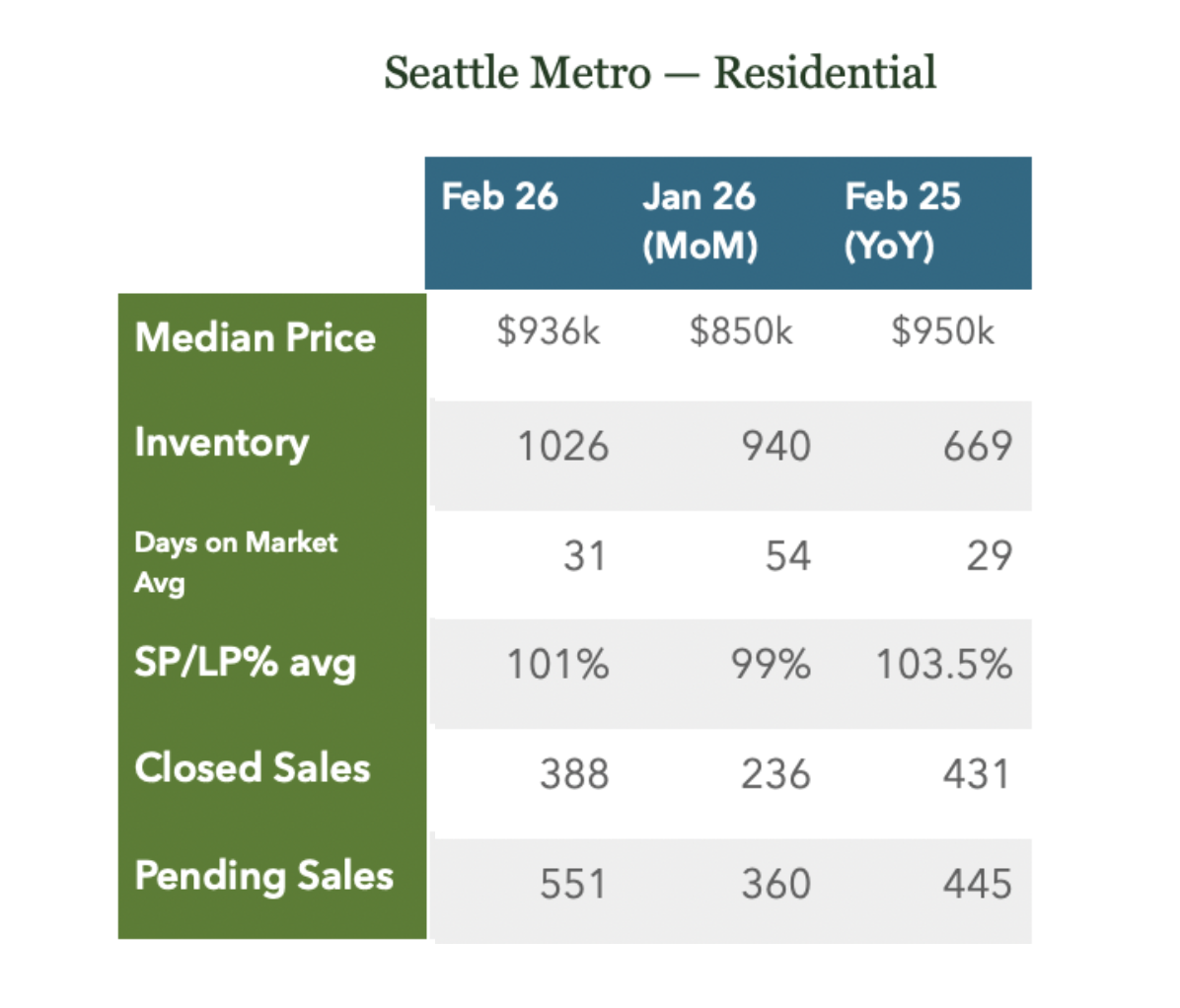

With clocks moving forward this weekend and Spring is just a couple of weeks away we are starting to see the Real Estate Market starting to form. We typically see signs right around the end of the Seahawks season and the Super Bowl, which matched up perfectly this year. This past February followed some seasonal trends of Month-to-Month rising prices, inventory and closed sales but a little off of a year ago. February is shorter month, so depending on where it starts and where it ends, it can sometimes influence Median and Closed final numbers. We do feel the market is picking up, but maybe not at the same pace as previous years (so far).

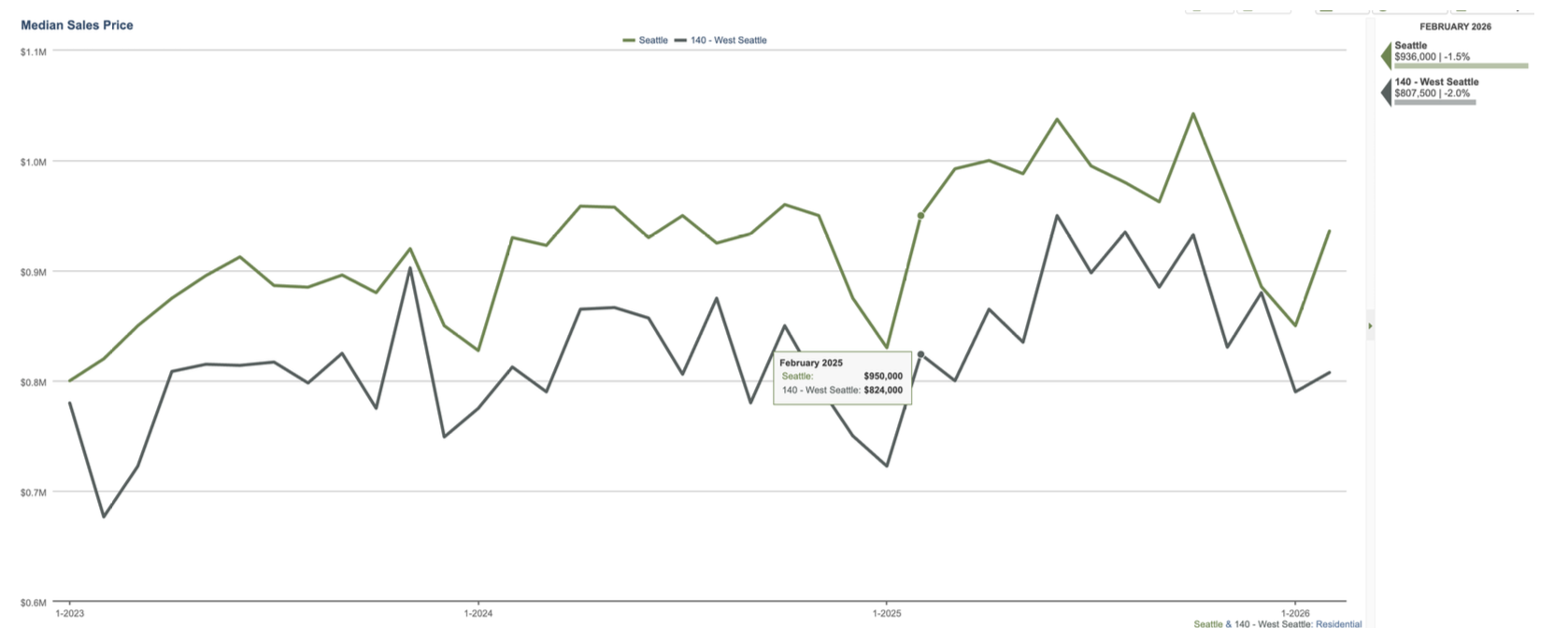

Median price usually dips in December and January and picks up in February. Median is based off closed sales is often a reflection of sales that went under contract the month before (which was up MoM but down YoY). And, with the shorter month we’ll probably have to wait another month to really see where the trend is going but right now it seems median should continue to build. Albeit, not at the same peaks of previous years. The thing we’ll have our eyes on is Sales Price/List Price ratios (how much did it sell over or under list). In many spring market, the higher escalator percentage pushes median price up. We are seeing and hearing of multiple offers with escalators, but maybe not the % over we have seen in previous years.

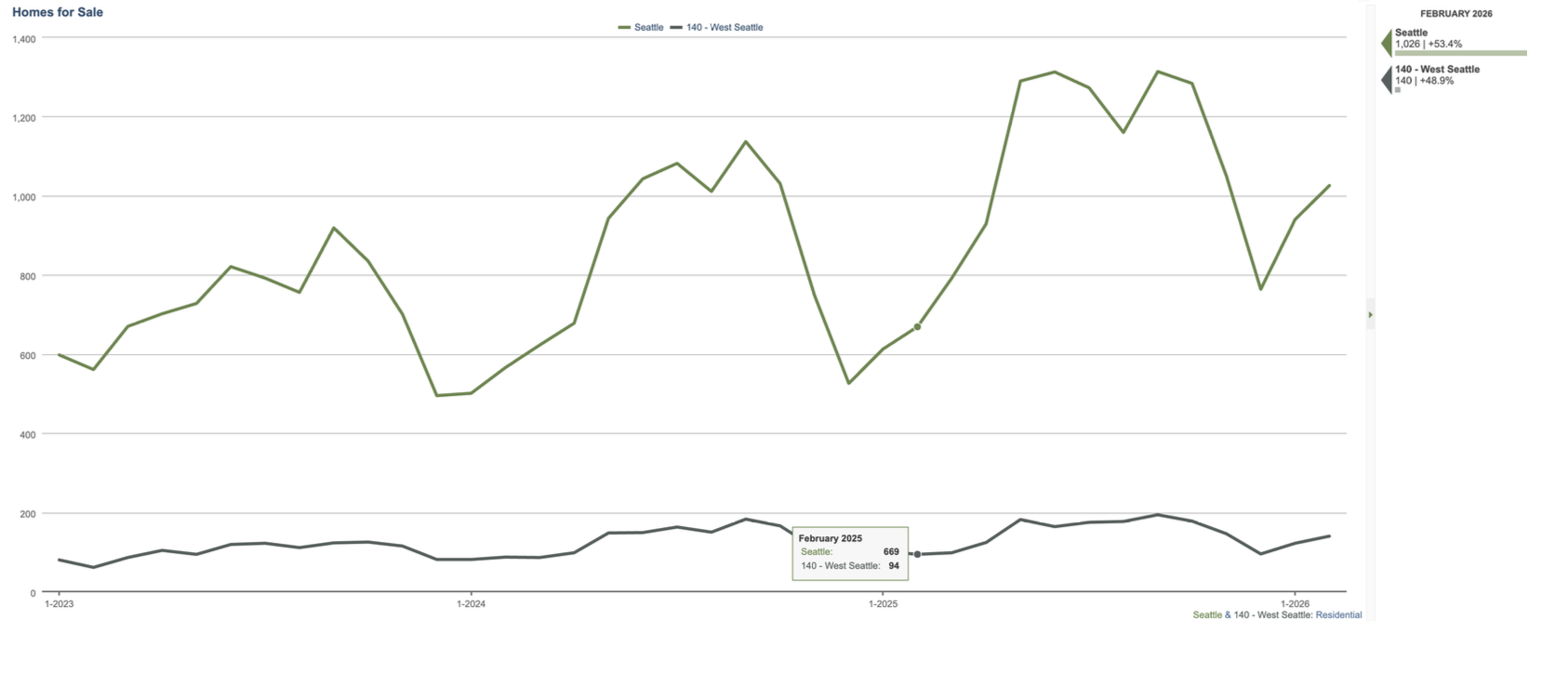

Inventory is starting its annual build up. We see dips in December and January as homes come off the market and are not replaced by new inventory. There were 24 New Listings last December vs. 122 last month. Sellers strategically list in better weather months and when there is less inventory/more demand. We would expect inventory to keep trickling out and New Listings peak in April and May. Also of note, 52 of the 140 residential homes For Sale are considered New Construction. So, these are likely New Homes, Townhomes, Back Yard Cottages, etc…. Previously owned homes (more traditional with year or earlier generation Townhome) levels are still pretty low.

Closed sales were slightly up for West Seattle and we’d expect that to continue next month. Closed sales are typically a reflection of the previous month’s Pending homes closing.

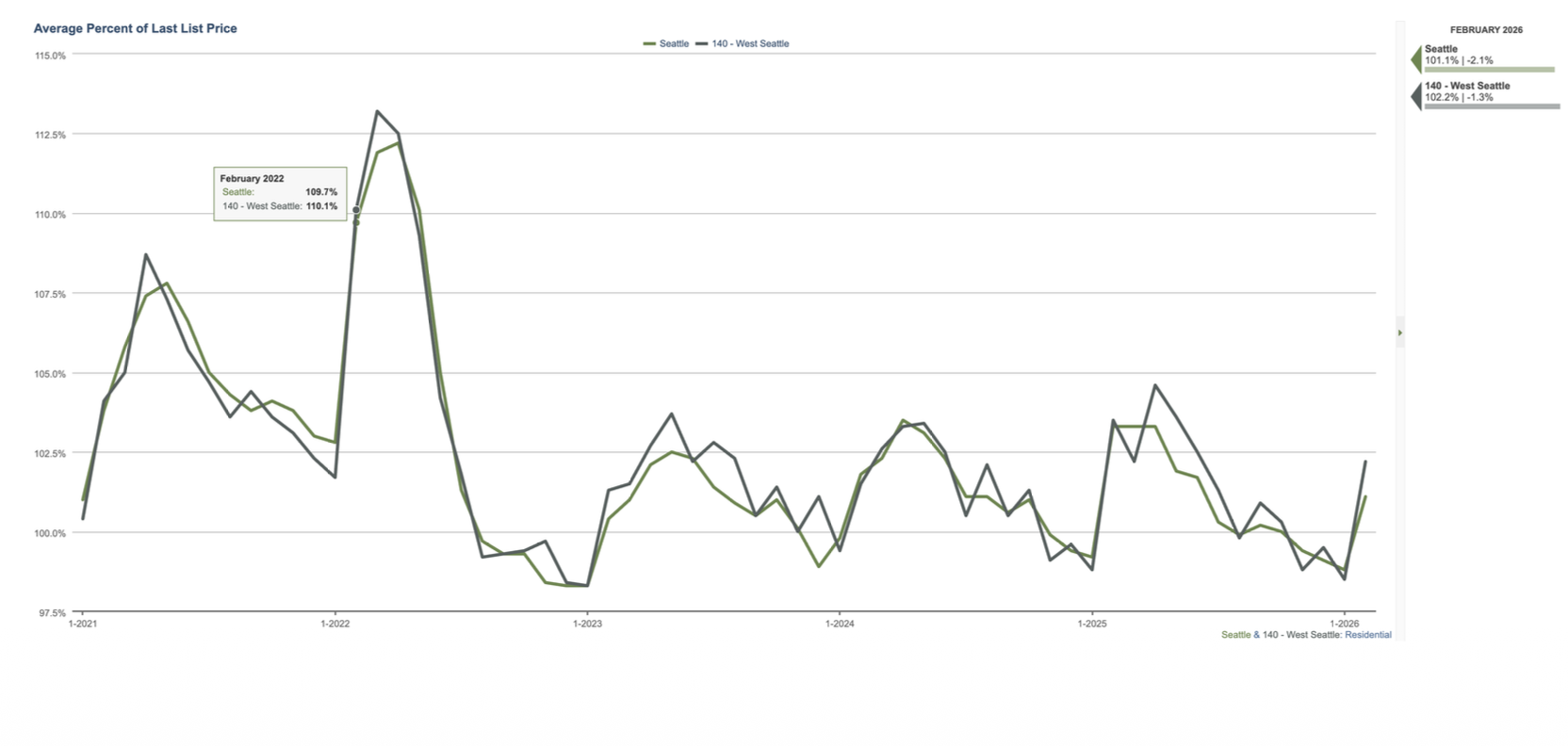

Here is a look at Sales Price/List Price ratios. While higher than the previous month, you can see how the compare to previous years. 2021 and 2022 were markets with lower interest rates, so buyers were much more aggressive with offers. We saw mortgage rates under 6% this past month, for the first time in years, but so far that has not transferred ridiculous escalators (on most houses). Big escalators are still happening for the right houses (see these two homes receiving over 20% of list). Of the 63 closed sales last month, 22 received over 100% of list, 14 received less than, and 27 received exactly.

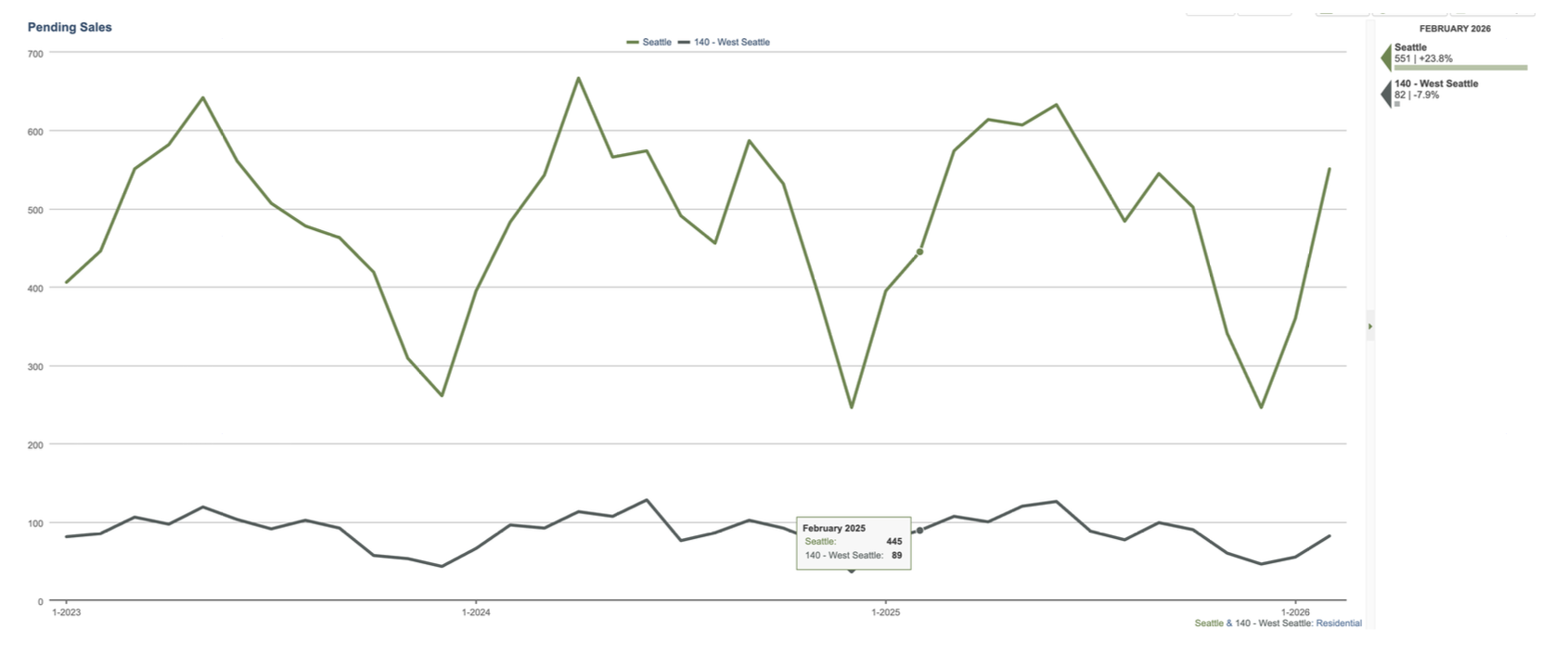

February was a shorter month, so not as many weeks for homes to go Pending, but shows overall improvement from previous month (Seattle Metro saw some big gains). We’d expect that to continue in March and April (despite World and Economic issues). These are the months that typically have the best inventory and the months buyers have targeted to purchase a house.

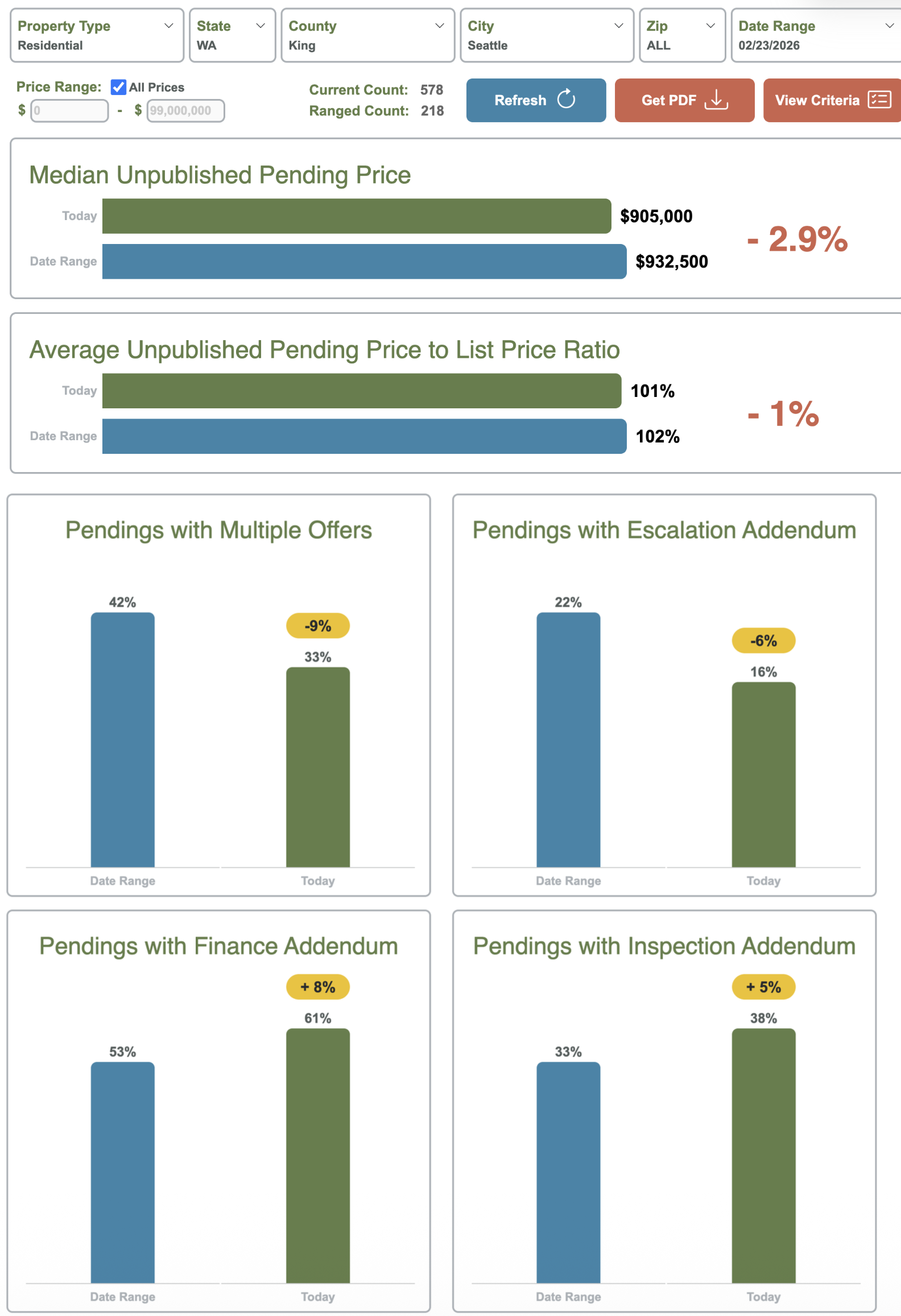

This takes a closer look at the Pending numbers for Seattle Metro. The take away here is there are less offers with multiple offers and escalators. And, we are seeing more Financing and Inspection Addendums. This will be interesting to watch as some of these numbers indicate a more balanced market. Still early though.

Seattle Metro numbers followed fairly typical seasonal trends (increase MoM but lower YoY) but will wait another month or so to gauge. It feels much like WS numbers, it’s picking up but not as crazy as past years.

Interest rates have been right at, or just under, 6% most of the month. However, we did see a slight uptick (up to 6.15%) over the weekend with the Iran war.